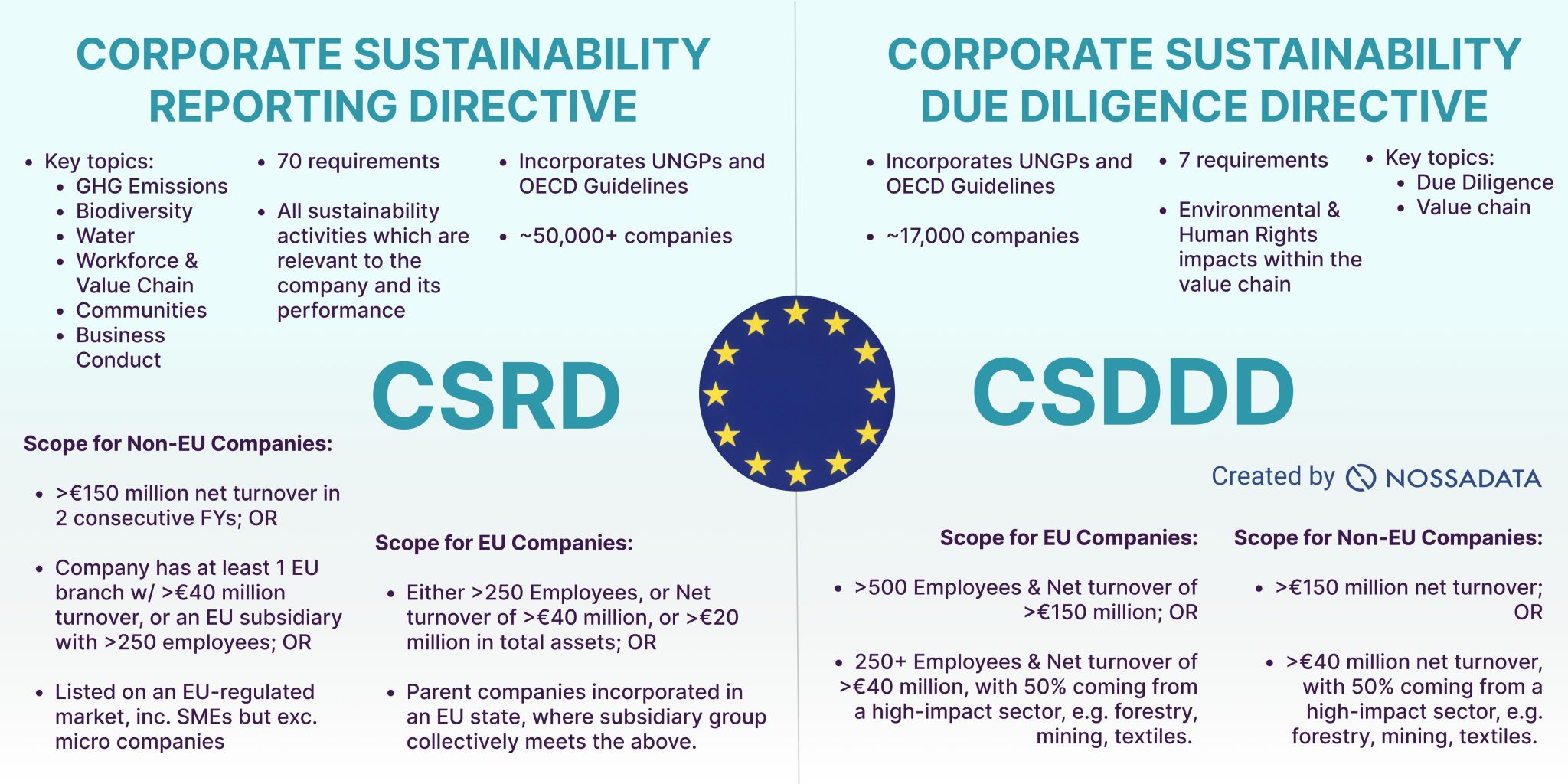

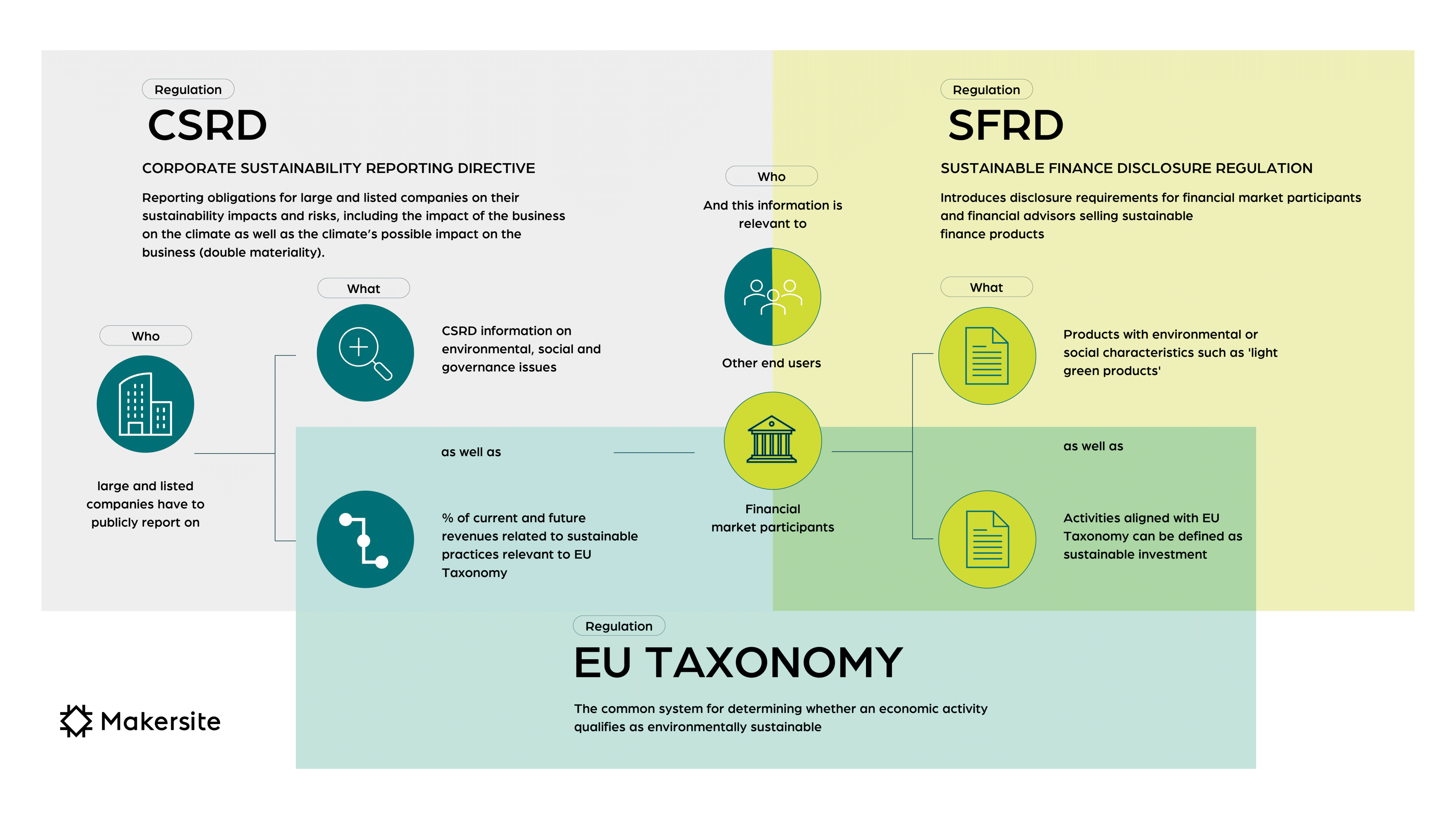

What is the CSRD The CSRD is European Union (EU) legislation, effective from 5 January 2023, that requires EU businesses—including qualifying EU subsidiaries of non-EU companies—to disclose their environmental and social impacts, and how their environmental, social and governance (ESG) actions affect their business.The EU Taxonomy defines economic activities that can be considered environmentally sustainable. The CSRD requires companies to report on their sustainability performance against the EU Taxonomy. The SFDR requires financial market participants to disclose how their products align with the EU Taxonomy.The CSRD applies to large companies based in the EU or with an annual turnover of above €150 million in the EU. What should be reported under CSRD

Does CSRD require scope 3 : In conclusion, the Corporate Sustainability Reporting Directive (CSRD) requires companies to report on scope 3 emissions, along with direct and indirect emissions.

What is the summary of CSRD requirements

The Corporate Sustainability Reporting Directive (CSRD) requires companies to report on the impact of corporate activities on the environment and society, and requires the audit (assurance) of reported information.

How do I prepare for CSRD : This guide covers five essential steps to start preparing for CSRD disclosure:

Understand your timeline & reporting level(s).

Assess what your company is required to report on.

Assemble the team.

Identify data gaps.

Go deep on climate.

The EU Taxonomy provides a classification system for sustainable economic activities that is applied within the CSRD and SFRD. The CSRD requires companies to publish sustainability metrics about their economic activities. For the first in-scope year, 2024, only large U.S. companies that are listed on an E.U.-regulated market and have more than 500 employees will be subject to the CSRD.

Does CSRD apply to non-EU companies

For non-EU companies or groups whose securities are admitted to trading on an EU-regulated market, application of the CSRD will occur progressively, starting from the 2024 financial year for those with (i) more than 500 employees and (ii) with more than €25m balance sheet total or more than €50m net turnover, with a …The CSRD, adopted by the European Commission at the end of 2022, substantially expands the number of companies covered, as well as the information they will be required to disclose on various environmental and social indicators, including climate.Mandatory reporting of Scope 3 emissions is already in place in Europe under the EU Corporate Sustainability Reporting Directive (CSRD). For non-EU companies or groups whose securities are admitted to trading on an EU-regulated market, application of the CSRD will occur progressively, starting from the 2024 financial year for those with (i) more than 500 employees and (ii) with more than €25m balance sheet total or more than €50m net turnover, with a …

Does CSRD require materiality assessment : CSRD requires companies to similarly assess the materiality of matters from an impact perspective, which considers the severity and likelihood of a company's impacts on society and the environment.

What are the CSRD reporting requirements : The Corporate Sustainability Reporting Directive (CSRD) requires companies to report on the impact of corporate activities on the environment and society, and requires the audit (assurance) of reported information.

What are the exemptions for CSRD

An exemption for subsidiaries

Subsidiaries are exempted from the CSRD obligations if the parent company produces a consolidated sustainability report that conforms with the CSRD. This subsidiary exemption also applies to subsidiaries that are public interest entities unless they reach the large company thresholds. The EU Corporate Sustainability Reporting Directive (CSRD) is a policy requiring large companies and public-interest entities operating in the EU to disclose information on their ESG performance annually.A double materiality assessment is the essential first step towards CSRD compliance that is needed so that organisations can focus their subsequent efforts on sustainability matters that are most relevant to them and their stakeholders.

What is required by the EU corporate sustainability reporting directive : Companies are to report on:

Environmental protection.

Social responsibility and treatment of employees.

Respect for human rights.

Anti-corruption and bribery.

Diversity on company boards (in terms of age, gender, educational and professional background)

![pochemu-sobaka-laet[1]](https://www.kysoh.com/wp-content/uploads/2024/06/pochemu-sobaka-laet1-1024x597-222x120.jpg)

![warum-hunde-heulen-01[1]](https://www.kysoh.com/wp-content/uploads/2024/06/warum-hunde-heulen-011-1024x683-222x120.jpg)

![719036743519[1]](https://www.kysoh.com/wp-content/uploads/2024/06/7190367435191-1024x568-222x120.jpg)

Antwort What are the requirements for CSRD in the EU? Weitere Antworten – What are the requirements for CSRD EU

What is the CSRD The CSRD is European Union (EU) legislation, effective from 5 January 2023, that requires EU businesses—including qualifying EU subsidiaries of non-EU companies—to disclose their environmental and social impacts, and how their environmental, social and governance (ESG) actions affect their business.The EU Taxonomy defines economic activities that can be considered environmentally sustainable. The CSRD requires companies to report on their sustainability performance against the EU Taxonomy. The SFDR requires financial market participants to disclose how their products align with the EU Taxonomy.The CSRD applies to large companies based in the EU or with an annual turnover of above €150 million in the EU. What should be reported under CSRD

Does CSRD require scope 3 : In conclusion, the Corporate Sustainability Reporting Directive (CSRD) requires companies to report on scope 3 emissions, along with direct and indirect emissions.

What is the summary of CSRD requirements

The Corporate Sustainability Reporting Directive (CSRD) requires companies to report on the impact of corporate activities on the environment and society, and requires the audit (assurance) of reported information.

How do I prepare for CSRD : This guide covers five essential steps to start preparing for CSRD disclosure:

The EU Taxonomy provides a classification system for sustainable economic activities that is applied within the CSRD and SFRD. The CSRD requires companies to publish sustainability metrics about their economic activities.

For the first in-scope year, 2024, only large U.S. companies that are listed on an E.U.-regulated market and have more than 500 employees will be subject to the CSRD.

Does CSRD apply to non-EU companies

For non-EU companies or groups whose securities are admitted to trading on an EU-regulated market, application of the CSRD will occur progressively, starting from the 2024 financial year for those with (i) more than 500 employees and (ii) with more than €25m balance sheet total or more than €50m net turnover, with a …The CSRD, adopted by the European Commission at the end of 2022, substantially expands the number of companies covered, as well as the information they will be required to disclose on various environmental and social indicators, including climate.Mandatory reporting of Scope 3 emissions is already in place in Europe under the EU Corporate Sustainability Reporting Directive (CSRD).

For non-EU companies or groups whose securities are admitted to trading on an EU-regulated market, application of the CSRD will occur progressively, starting from the 2024 financial year for those with (i) more than 500 employees and (ii) with more than €25m balance sheet total or more than €50m net turnover, with a …

Does CSRD require materiality assessment : CSRD requires companies to similarly assess the materiality of matters from an impact perspective, which considers the severity and likelihood of a company's impacts on society and the environment.

What are the CSRD reporting requirements : The Corporate Sustainability Reporting Directive (CSRD) requires companies to report on the impact of corporate activities on the environment and society, and requires the audit (assurance) of reported information.

What are the exemptions for CSRD

An exemption for subsidiaries

Subsidiaries are exempted from the CSRD obligations if the parent company produces a consolidated sustainability report that conforms with the CSRD. This subsidiary exemption also applies to subsidiaries that are public interest entities unless they reach the large company thresholds.

The EU Corporate Sustainability Reporting Directive (CSRD) is a policy requiring large companies and public-interest entities operating in the EU to disclose information on their ESG performance annually.A double materiality assessment is the essential first step towards CSRD compliance that is needed so that organisations can focus their subsequent efforts on sustainability matters that are most relevant to them and their stakeholders.

What is required by the EU corporate sustainability reporting directive : Companies are to report on: